1Independent Climatologist, Economist, Membrane Institute, USA

2Independent Physicist, Membrane Institute, USA

Sidd said: “frightening article by Jeff Masters. We saw some of this coming, the flood risk aint just along the coast, it extends 100 miles inland… the water cant get out …”

https://yaleclimateconnections.org/2026/08/the-floods-of-the-future-wont-come-one-at-a-time/

In the 1990s, Sidd and I began developing real-estate-based climate risk models. From the beginning, one of the underlying high-risk factors was flooding—and, closely linked to it, the availability and affordability of flood insurance. In the early 2000s, we met with FEMA, Fannie Mae (FNMA), and Freddie Mac (FHLMC) to better understand their flood-risk modeling and emerging plans for managed retreat.

In October 2023, Sidd observed: “Now I am thinking the violent rain will be a bigger problem before we die.”

That concern has become increasingly relevant. As the Earth warms, warmer air can physically hold more water vapor than cooler air. For every 1°C (1.8°F) increase in temperature, the atmosphere can hold approximately 7% more moisture, increasing the potential for extreme precipitation. Over a 10°C increase, atmospheric moisture-holding capacity would nearly double, creating the potential for substantially more intense rainfall.

The problem, however, is not simply the amount of water falling from the sky. It is also what happens when that water moves across the landscape—and whether infrastructure and government response systems are capable of managing, containing, and recovering from the resulting flows.

Flow forces scale with the square of velocity (v²). As flow speeds increase—whether from heavier rainfall, steeper runoff, or more intense hydrological events—the destructive force of moving water rises rapidly. Density further magnifies this effect. Water is roughly 800 times denser than air, meaning that a comparable flow velocity can produce dramatically greater force.

Together, we developed a series of models incorporating the Clausius–Clapeyron relationship, the extreme energy transfer within the water cycle through latent heat, and fluid-flow dynamics. These models increasingly pointed toward a risk structure in which flooding could no longer be treated as an isolated coastal problem. Instead, precipitation intensity, runoff, topography, infrastructure vulnerability, insurance stress, and limited recovery capacity can interact and compound one another across much larger regions.

By 2026, the framework had evolved from a theoretical real-estate climate-risk model into a broader multiplicative risk framework that could be evaluated against observed real-world conditions.

The latest evolution of this work is presented in the following three papers:

Insurance markets are among the first financial systems to directly price climate risk. As extreme weather events become more frequent, severe, and costly, insurers are raising premiums, reducing coverage, and withdrawing from high-risk regions altogether. This growing insurance crisis extends beyond individual property owners. Insurance underpins mortgage lending, infrastructure investment, and long-term capital formation. When insurance becomes unaffordable or unavailable, the economic consequences can cascade through entire financial systems.

Emerging evidence suggests that continued warming beyond approximately 2–3°C above pre-industrial levels could render broad classes of physical assets partially or wholly uninsurable. In this sense, the insurance industry may represent one of the earliest indicators of systemic climate instability.

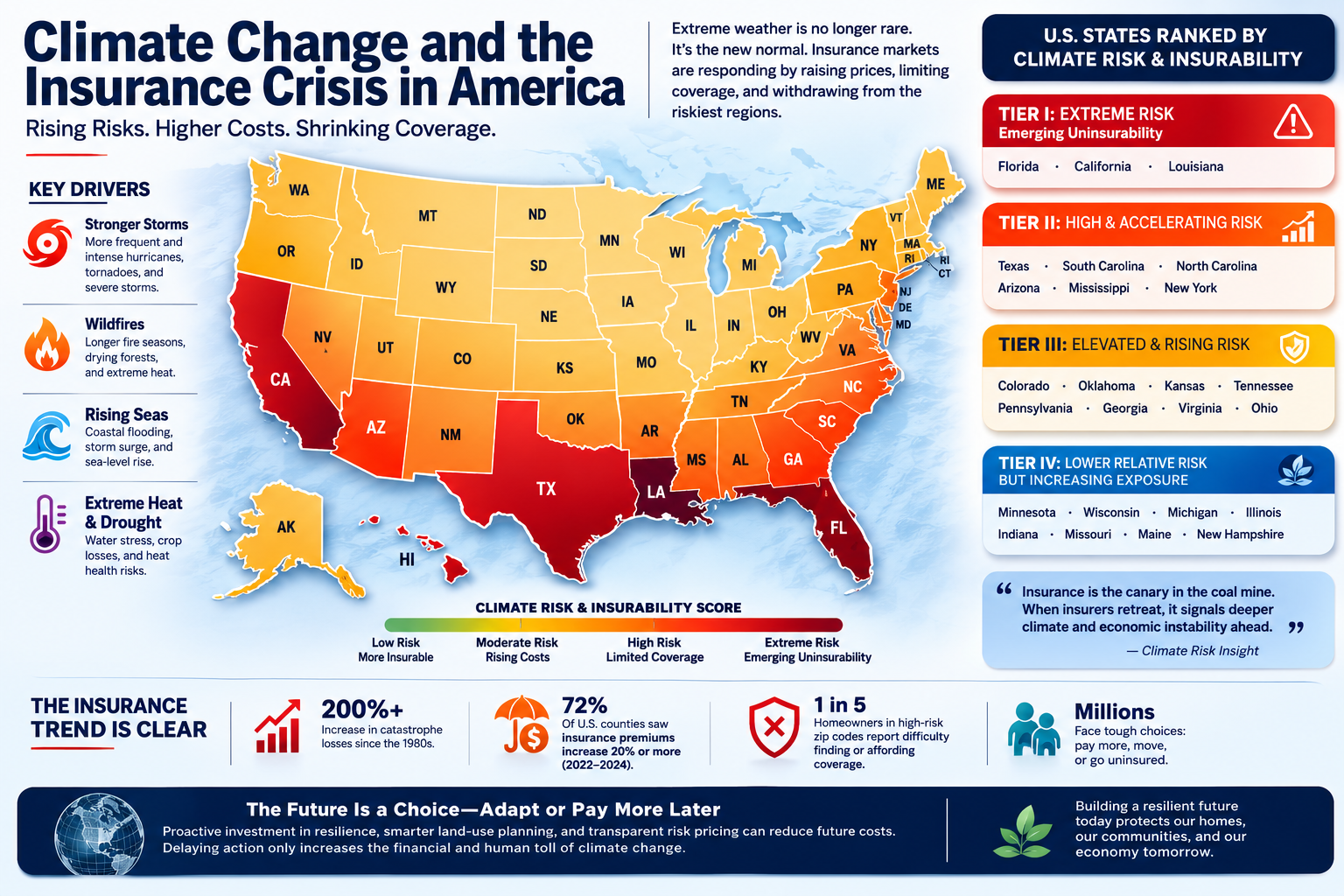

Climate risks are not evenly distributed across the United States. Some states are experiencing rapidly accelerating exposure to hurricanes, sea-level rise, extreme heat, wildfires, drought, inland flooding, and severe convective storms. These hazards are increasingly reflected in insurance premiums, declining policy availability, and the withdrawal of private insurers from high-risk markets.

The following rankings represent a qualitative assessment of states based on three primary factors:

| State | Primary Climate Risks | Insurance Conditions |

|---|---|---|

| Florida | Hurricanes, storm surge, sea-level rise, extreme rainfall, flooding, and extreme heat | Rapid premium increases, insurer withdrawals, reduced private-market capacity, and heavy reliance on Citizens Property Insurance Corporation |

| Louisiana | Hurricanes, coastal flooding, land subsidence, sea-level rise, and extreme rainfall | Severe market contraction, insurer withdrawals, rising premiums, and escalating affordability crisis |

| California | Wildfires, drought, extreme heat, flooding, and severe storms | Major insurer withdrawals, expanding FAIR Plan exposure, tightening underwriting standards, and rapidly increasing premiums |

| Texas | Hurricanes, extreme rainfall, flooding, hailstorms, tornadoes, extreme heat, and drought | Rapidly rising premiums, increasing catastrophe losses, insurer risk reduction, and growing affordability concerns |

| Hawaii | Wildfire, sea-level rise, coastal flooding, erosion, hurricanes, extreme rainfall, drought, and ecosystem loss | Rising premiums, insurer capacity constraints, increasing wildfire exposure, and growing availability concerns in high-risk areas |

| South Carolina | Hurricanes, storm surge, sea-level rise, extreme rainfall, coastal flooding, and heat | Rising premiums, increasing catastrophe exposure, tightening coastal underwriting, and growing availability concerns |

| North Carolina | Hurricanes, coastal flooding, extreme rainfall, inland flooding, and severe storms | Rising premiums, increasing reinsurance costs, growing coastal insurance pressures, and emerging availability constraints |

| New Jersey | Sea-level rise, coastal flooding, nor'easters, storm surge, and increasingly intense rainfall | Rapidly rising premiums, increasing flood insurance costs, and emerging availability constraints in high-risk coastal areas |

| Delaware | Sea-level rise, chronic tidal flooding, saltwater intrusion, hurricane exposure, and coastal erosion | Rising insurance costs and growing affordability concerns driven by escalating coastal flood risk |

These states represent the leading edge of America's insurance crisis. Multiple climate hazards are converging with rising reconstruction costs, causing portions of their insurance markets to exhibit characteristics of emerging uninsurability.

| Alabama | Hurricanes, tornadoes, extreme precipitation, inland flooding, heat, and coastal storm surge | Rising insurance costs, increasing catastrophe exposure, and growing affordability and availability concerns in high-risk areas |

| Virginia | Sea-level rise, land subsidence, coastal flooding, inland flooding, and hurricane-related precipitation | Rising insurance costs, increasing flood exposure, and growing long-term insurability concerns in vulnerable coastal regions |

| Georgia | Hurricanes, coastal storm surge, extreme precipitation, inland flooding, severe convective storms, tornadoes, and extreme heat | Rising premiums, increasing catastrophe losses, and growing affordability concerns in coastal and high-risk areas |

| Colorado | Wildfires, drought, extreme heat, water stress, hailstorms, and severe storms | Rising premiums, wildfire-related insurance pressure, and increasing underwriting restrictions in high-risk areas |

| New York | Coastal flooding, extreme precipitation, heat, inland flooding, and severe storms | Rising insurance costs, increasing catastrophe exposure, and growing long-term insurability concerns in high-risk coastal and flood-prone areas |

| Arizona | Extreme heat, drought, water stress, wildfires, and extreme rainfall | Rising insurance costs and growing long-term insurability concerns driven by heat, water, and wildfire risks |

| Missouri | Extreme precipitation, inland flooding, severe convective storms, tornadoes, heat, and drought | Rising premiums, increasing catastrophe losses, and growing market stress driven by repetitive severe weather events |

| Oregon | Wildfires, drought, extreme heat, flooding, and severe storms | Rising premiums, increasing wildfire exposure, and growing availability concerns in high-risk areas |

| Washington | Wildfires, extreme heat, flooding, drought, and severe storms | Increasing catastrophe losses, rising premiums, and emerging insurance availability concerns |

| Nevada | Extreme heat, drought, water stress, wildfires, and extreme rainfall | Rising insurance costs and growing climate-driven affordability concerns |

These states remain largely insurable but are experiencing accelerating climate pressures that are increasing financial losses and straining traditional risk-pricing models.

| State | Primary Climate Risks | Insurance Conditions |

|---|---|---|

| Tennessee | Extreme precipitation, flooding, severe storms, tornadoes, and heat | Rising claims, increasing premiums, and growing catastrophe losses |

| Oklahoma | Hailstorms, tornadoes, drought, and severe convective storms | Persistent premium increases, high claim frequency, and increasing underwriting pressure |

| Kansas | Hailstorms, drought, extreme weather, and severe convective storms | Increasing insurance costs, higher loss ratios, and rising catastrophe exposure |

| Pennsylvania | Extreme precipitation, inland flooding, heat waves, and severe storms | Moderate but accelerating insurance costs and increasing flood-related losses |

| Maryland | Coastal flooding, sea-level rise, Chesapeake Bay impacts, extreme rainfall, and storms | Rising premiums and increasing flood-related insurance pressure |

| Connecticut | Coastal flooding, hurricanes, extreme precipitation, and storms | Increasing premiums and growing coastal insurance concerns |

| Massachusetts | Coastal flooding, sea-level rise, extreme storms, and precipitation | Rising coastal insurance costs and increasing climate-related losses |

| Ohio | Flooding, severe storms, tornadoes, and extreme heat | Rising premiums and increasing severe-weather losses |

| Illinois | Flooding, extreme heat, severe storms, and heavy precipitation | Increasing catastrophe losses and gradual insurance cost escalation |

| Michigan | Extreme precipitation, flooding, heat, and severe storms | Rising claims and increasing climate-related insurance pressure |

Even states historically viewed as relatively safe—including portions of the Upper Midwest and New England—are experiencing increasing exposure to flooding, severe precipitation events, heat waves, and infrastructure stresses associated with climate change. While insurance markets in these regions remain comparatively stable, long-term trends suggest that no state is entirely insulated from accelerating climate risks.

The geographic boundaries of insurability are increasingly being redrawn by climate change. Insurance markets are repricing risks faster than most real estate markets and government policies can adapt. States experiencing multiple, compounding climate hazards are likely to encounter higher premiums, reduced availability of coverage, increasing dependence on state-backed insurance mechanisms, and growing pressure for adaptation and managed retreat.

The insurance industry may therefore be functioning as an early warning system, identifying regions where accelerating climate risks are beginning to exceed the financial assumptions upon which modern property markets have long depended.

Florida's state-backed insurer, Citizens Property Insurance Corporation, has become the state's largest property insurer as private companies retreat from the market in response to escalating hurricane risks and mounting losses.

Although Citizens serves as a critical safety net, it faces significant financial pressures. The increasing frequency and severity of hurricanes make maintaining long-term solvency increasingly difficult without substantial taxpayer support.

Citizens operates under a unique structure in which major losses can trigger statewide assessments on policyholders, including those insured by private carriers. As powerful storms become more destructive, these assessments could rise to unsustainable levels, placing increasing financial burdens on Florida residents.

The instability of Florida's insurance market exposes broader vulnerabilities within the state's real estate sector.

As storms intensify and reconstruction costs soar, property values in high-risk coastal regions face growing downward pressure. Rising insurance premiums and declining availability of coverage increasingly challenge the long-term viability of owning property in vulnerable areas.

Managed retreat—the strategic relocation of communities and investments away from high-risk regions—is becoming an increasingly important policy consideration.

Rising global temperatures, changing weather patterns, sea-level rise, and increasing storm-surge risks are amplifying losses across Florida's economy.

Improving resilience through stronger building codes, elevated infrastructure, improved stormwater management systems, and enhanced emergency preparedness will be essential. However, adaptation measures alone may not fully offset rapidly escalating climate risks.

Policymakers, insurers, and property owners must confront the growing mismatch between rising climate risks and the traditional insurance model.

Diversifying local economies, investing in resilient infrastructure, and exploring innovative risk-sharing mechanisms may help reduce vulnerabilities. Without meaningful adaptation and emissions reductions, the combined financial strain on insurers, taxpayers, and property owners could become increasingly difficult to sustain.

For some communities and investors, difficult decisions regarding relocation and managed retreat may become unavoidable.

Large portions of California, particularly wildfire-prone regions, face increasing risks from intensifying climate extremes. Wildfires, prolonged droughts, extreme heat, and episodic flooding are placing growing stress on both ecosystems and human settlements.

As climate conditions become increasingly favorable for large, fast-moving fires, questions arise regarding the long-term sustainability of rebuilding in repeatedly affected regions.

Wildfires leave behind extensive environmental damage that extends beyond the immediate destruction of homes and infrastructure.

Post-fire landscapes can contain ash, heavy metals, combustion byproducts, and other contaminants that complicate recovery efforts and may pose long-term health risks. Rebuilding communities in severely damaged areas often requires extensive remediation and significant investment.

California is among several states experiencing growing financial strain from climate-driven disasters.

Catastrophic wildfires and other extreme weather events have generated mounting losses for insurers. In response, several private insurers have reduced their exposure by limiting new policies or withdrawing from high-risk markets.

As private options diminish, increasing numbers of homeowners have turned to the state's FAIR Plan.

Originally intended as a temporary safety net, the FAIR Plan has experienced rapid growth as more properties become difficult or impossible to insure through traditional markets.

This expanding exposure significantly increases the plan's vulnerability to catastrophic losses.

California has recently amended insurance regulations to allow insurers greater flexibility in pricing catastrophic risks.

While these changes may encourage insurers to remain in the market, they also raise significant concerns about affordability. Many homeowners in high-risk regions may ultimately find coverage prohibitively expensive or unavailable.

Major wildfires in the Los Angeles region continue to test the resilience of both the FAIR Plan and California's broader insurance framework.

Several factors contribute to escalating losses:

These forces are simultaneously increasing both claim frequency and claim severity.

As climate risks continue to intensify, managed retreat—the strategic relocation of communities, infrastructure, and investment away from high-risk areas—may increasingly become a practical adaptation strategy.

Communities, policymakers, insurers, and investors face difficult questions:

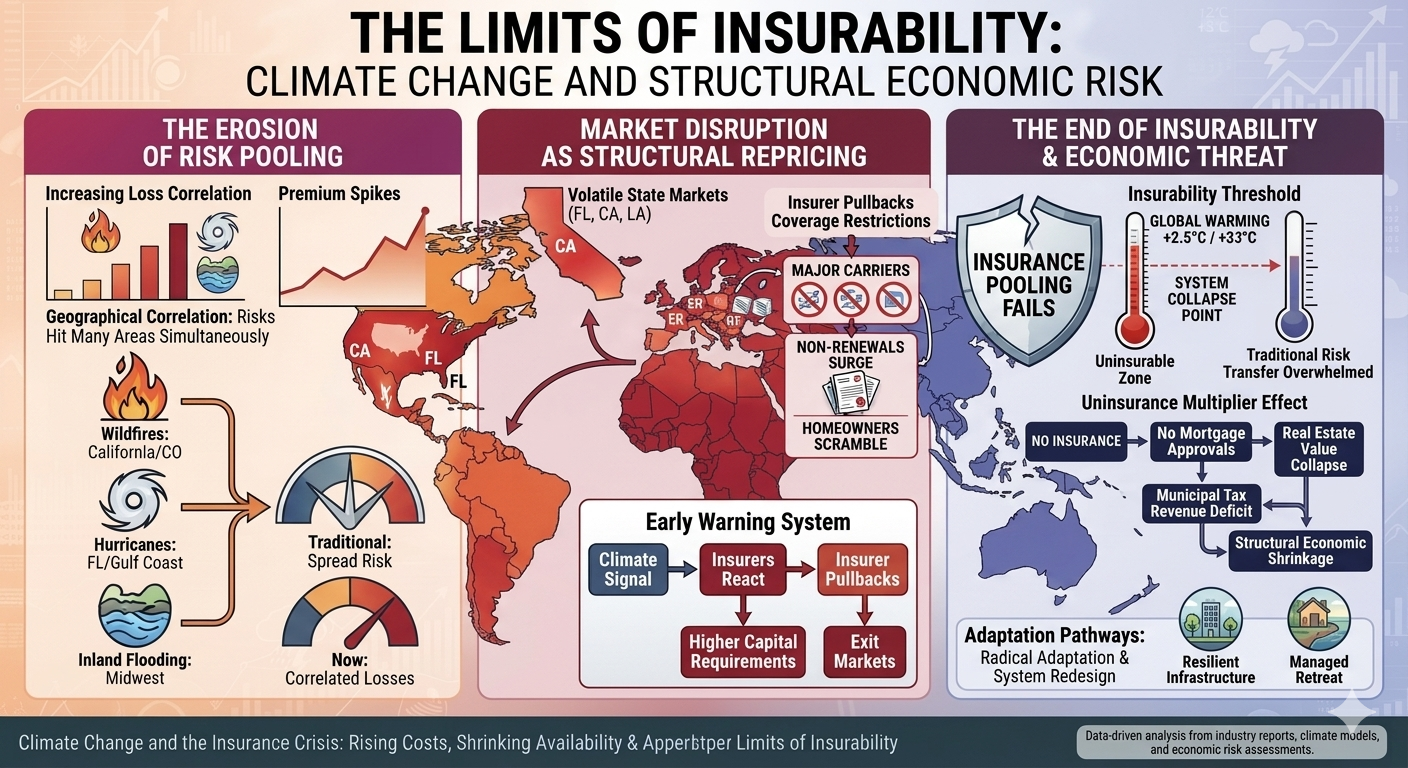

Insurance functions by spreading risk across large populations and assuming that losses remain sufficiently unpredictable and financially manageable. Climate change challenges these assumptions.

When extreme events become increasingly frequent, severe, and geographically widespread, risk pooling becomes more difficult and premiums rise accordingly. In the most vulnerable regions, coverage may become prohibitively expensive or disappear altogether.

The insurance crisis emerging in states such as Florida, California, and Louisiana may therefore represent more than a temporary market disruption. It may signal the early stages of a broader repricing of climate risk across modern economies.

Insurance markets are acting as an early warning system. Their response suggests that climate risk is increasingly becoming a structural economic challenge rather than merely an environmental issue. The trajectory of future warming will help determine whether insurance remains a viable mechanism for managing risk—or becomes one of the first major institutions fundamentally constrained by accelerating climate change.

Climate change is fundamentally destabilizing insurance markets by driving increasingly severe financial losses, pushing premiums sharply higher, and causing insurers to reduce or withdraw coverage in some high-risk regions. As extreme weather events become more frequent and, in many cases, more intense, traditional underwriting models are being challenged by rapidly changing risk. The result is a growing transfer of financial risk from private insurers to consumers, businesses, lenders, and governments.

One of the clearest signs of growing insurance instability is the widening protection gap—the difference between total economic losses from disasters and the portion covered by insurance.

In many climate-vulnerable regions, the majority of disaster losses remain uninsured. The gap can be particularly severe in developing economies, where insurance penetration is low and households, businesses, and governments may lack the financial resources to recover from catastrophic events.

This creates a dangerous feedback loop:

More extreme losses → higher insurance costs → reduced coverage → greater uninsured losses → greater financial vulnerability

The protection gap is therefore not simply an insurance problem. It is increasingly a problem of household financial security, economic resilience, infrastructure recovery, and public finance.

Insurers are increasingly reassessing their exposure to regions where climate-related risks are becoming more difficult to price and manage.

In some high-risk markets, major insurers have stopped writing certain types of new business, declined to renew policies, restricted coverage, increased deductibles, or imposed substantially higher premiums. These trends have been especially visible in wildfire-prone areas of California and hurricane- and flood-exposed coastal regions.

When private carriers retreat, governments and state-sponsored insurance programs often become insurers of last resort. This can concentrate risk in public or quasi-public systems while leaving taxpayers increasingly exposed to catastrophic losses.

Property insurance is closely connected to the housing and banking systems because mortgage lenders generally require borrowers to maintain adequate insurance on the underlying property.

As premiums rise and coverage becomes more difficult to obtain, homeowners can face rapidly increasing housing costs even when their mortgage payment remains unchanged. In the most exposed markets, some properties may become effectively uninsurable or prohibitively expensive to insure.

This creates a potential chain reaction:

Climate risk → higher insurance costs → declining property affordability → falling property values → mortgage stress → increased financial-system risk

The burden can fall disproportionately on lower-income homeowners, who have less capacity to absorb sudden increases in insurance and other climate-related costs.

Rising insurance premiums can also contribute to broader economic volatility. Insurance is an input into housing, transportation, agriculture, construction, business operations, and investment.

When insurers raise premiums to reflect increased catastrophe risk, those costs can eventually be passed through to consumers in the form of higher rents, housing costs, food prices, transportation costs, and prices for other goods and services.

In particularly vulnerable areas, insurance costs can also influence where people are willing and able to live. If housing becomes prohibitively expensive to insure—or insurance becomes unavailable altogether—households and businesses may begin relocating toward less exposed regions.

Climate change can therefore contribute to climate-driven migration within countries and across regions, even before an area becomes physically uninhabitable.

The global property and casualty (P&C) insurance market is experiencing very different levels of stress depending on regional climate hazards, catastrophe exposure, insurance penetration, regulatory frameworks, and the capacity of governments to absorb residual risk.

The following ranking identifies major regions experiencing significant climate-driven insurance disruption, moving from the most acute and visible market stress toward regions where systemic pressures are emerging or are likely to intensify.

| Global Rank | Vulnerable Region | Key Impacted Areas | Primary Climate Perils | Market Disruption Level | Key Insurance Market Impact |

|---|---|---|---|---|---|

| 1 | North America | Florida; California; Gulf Coast | Hurricanes, wildfires, severe convective storms, flooding | Critical | Major premium increases, restricted coverage, insurer withdrawals from selected markets, rising reliance on state-backed insurers and residual-market programs |

| 2 | Europe | Mediterranean coast; Central European flood basins | Extreme heat, wildfires, flooding, severe storms | Severe | Growing protection gaps in high-risk areas, rising catastrophe and reinsurance costs, increasing pressure on household and commercial insurance |

| 3 | Asia-Pacific | Coastal China; Japan; eastern Australia | Typhoons, sea-level rise, flooding, bushfires | High | Increasing pressure on property and agricultural insurance, growing exposure of ports, supply chains, and coastal infrastructure |

| 4 | Latin America & Caribbean | Caribbean island nations; coastal Mexico | Hurricanes, flooding, drought, extreme heat | Moderate to High | Large uninsured disaster losses, limited insurance penetration, and growing dependence on international reinsurance and alternative risk-transfer mechanisms |

| 5 | Sub-Saharan Africa | East African Rift; southern African coastal zones | Multi-year droughts, flooding, extreme heat, severe storms | Emerging Systemic Risk | Very low insurance penetration in many markets, substantial reliance on microinsurance, development finance, humanitarian assistance, and international climate-risk mechanisms |

The geographic details differ, but the underlying pattern is increasingly similar:

Climate risk rises → catastrophe losses increase → insurers reassess risk → premiums rise or coverage contracts → the protection gap widens → households, businesses, and governments absorb more of the loss.

This represents a fundamental challenge to the traditional concept of insurability.

Insurance works most effectively when risks are sufficiently predictable, geographically diversified, and economically manageable. Climate change can undermine all three conditions simultaneously. When catastrophic risks become correlated across large geographic areas, historical loss data become less reliable as a guide to future exposure, and the cost of transferring risk through reinsurance increases.

The consequences extend well beyond the insurance industry.

A property that cannot be affordably insured can become difficult to finance. A home that cannot be financed can lose market value. A business that cannot obtain affordable coverage can become less competitive or relocate. A community facing repeated disasters can experience declining tax revenues while public recovery costs rise.

The insurance market is therefore becoming an increasingly important early-warning indicator of climate-driven financial stress.

What begins as a change in weather risk can ultimately become a problem involving housing, banking, inflation, public budgets, infrastructure, migration, and regional economic stability.

The question is no longer simply whether climate change is generating larger physical losses.

It is whether the global financial system can continue to price, distribute, and absorb those losses at a sustainable cost.

Bottom line: The question is no longer how warm the planet becomes, but how life on Earth can endure when change outpaces our ability to adapt.

We cannot control the laws of physics, but we can control our pollution. The most effective action is to stop burning fossil fuels.